Market View Monthly - Economic Review

Equities pulled back in June, despite further progress towards a resolution in the Middle East, and the excitement around the largest Initial Public Offering (IPO) in history, SpaceX. Investors were concerned about lofty valuations ahead of earnings season in sectors like Technology and Communication Services, and some skepticism about the artificial intelligence (AI) trade seeped back into the market. Despite this, value stocks, and small cap stocks both performed well on the month and continue to lead through the first half of 2026.

Economic Review¹

The US economy added 172K jobs in May 2026, well above forecasts of 85K, continuing to point to a resilient labor market. The unemployment rate remained at 4.3%, signaling that AI is not causing layoffs at a noticeable scale.

Job openings expanded meaningfully to 8.18 million, meaning that for every unemployed person there are 1.2 jobs available.

The ISM Manufacturing PMI expanded for a 5th month in a row, rising to 54.0, which was the highest reading since May of 2022. The index continues to signal expansion in the manufacturing sector, a sign that a rebound may be underway.

The prices paid index remains elevated at 82.1 but was slightly lower than previous levels.

The ISM Non-Manufacturing (Services) Index also moved higher, rising to 54.5, above forecasts of 53.8.

The Consumer Price Index (CPI) rose 4.2% on a year-over-year (YoY) basis in May of 2026, which was the highest level since April of 2023. The index rose 0.5% month-over-month (MoM), which was the lowest since February.

Core CPI, which excludes food and energy, rose only 0.2% in May and is up 2.9% over the last year.

Much of the increase was linked to rising airfares, which are tied to energy prices.

The U.S. Producer Price Index (PPI) rose 1.1% MoM in May, the second consecutive month with a rise above 1% on a monthly basis. The index is up 6.5% YoY.

Core PPI, which excludes the volatile food and energy categories, rose 0.4% in May but remains up 4.9% YoY.

U.S. Retail Sales rose 0.9% in quelling concerns of a weakening consumer. The figure rose 6.9% YoY.

Excluding gasoline stations, which are dominated by rising energy prices, the reading came in at 0.7%, a commendable reading.

The University of Michigan Consumer Sentiment Index bounced off its record lows, coming in at 48.9 in June, likely reflecting some relief in lower gas prices.

In a rare reading, consumers began pricing in improved future expectations from their current conditions.

Kevin Warsh had his first press conference as Federal Reserve (Fed) Chairman after the committee decided to hold rates at their current level. He noted that the Fed would be looking at an array of issues like how to communicate with the press, how to view the balance sheet, and how to view inflation best.

The Personal Consumption Expenditures Price Index (PCE) increased 0.4% in May, lifting the annual inflation rate to 4.1%, its first time passing 4% since 2023.

Core PCE, which removes the volatile food and energy categories, increased 0.3% in May and remained elevated at 3.4% over the past year.

Real Gross Domestic Product (GDP) growth was revised higher to a 2.1% annualized rate in the final estimate for Q1, up from the 1.6% previously reported.

Monthly Insight:

June’s array of data that was released painted a picture of a resilient consumer, and growing economy. Retail sales and GDP continued to churn higher, and the consumer continues to spend and remain employed despite rising inflation as a headwind to the consumer. The pickup in manufacturing also boded well for growth and could be a leading indicator for the buildout of AI infrastructure. The probability for a Fed rate hike rose in the month of June, in lockstep with the rising concern of inflation, but so far the Fed has not pointed towards a rate hike, and inflation has remained relatively contained to energy prices. However, with the labor market in a strong position, the Fed will likely be squarely focused on their second half of the mandate, inflation.

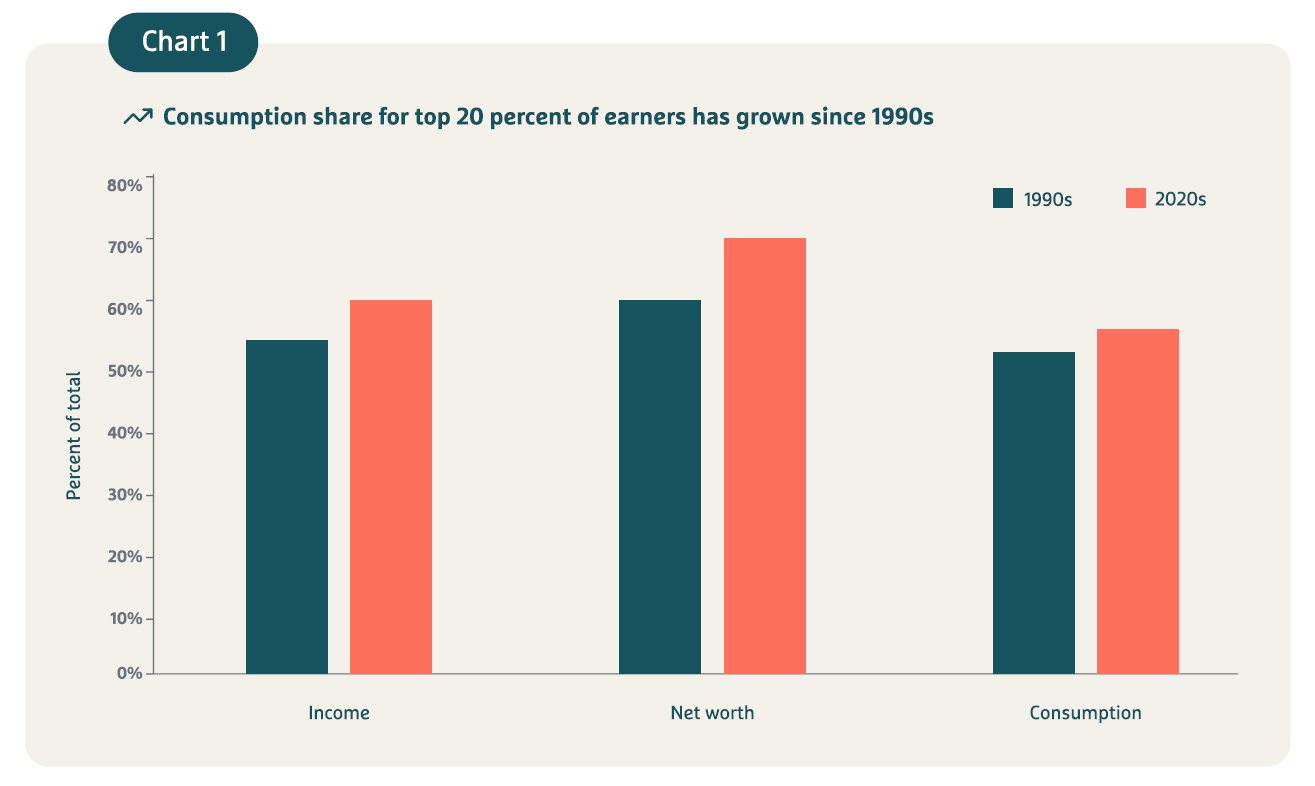

Chart of the Month²

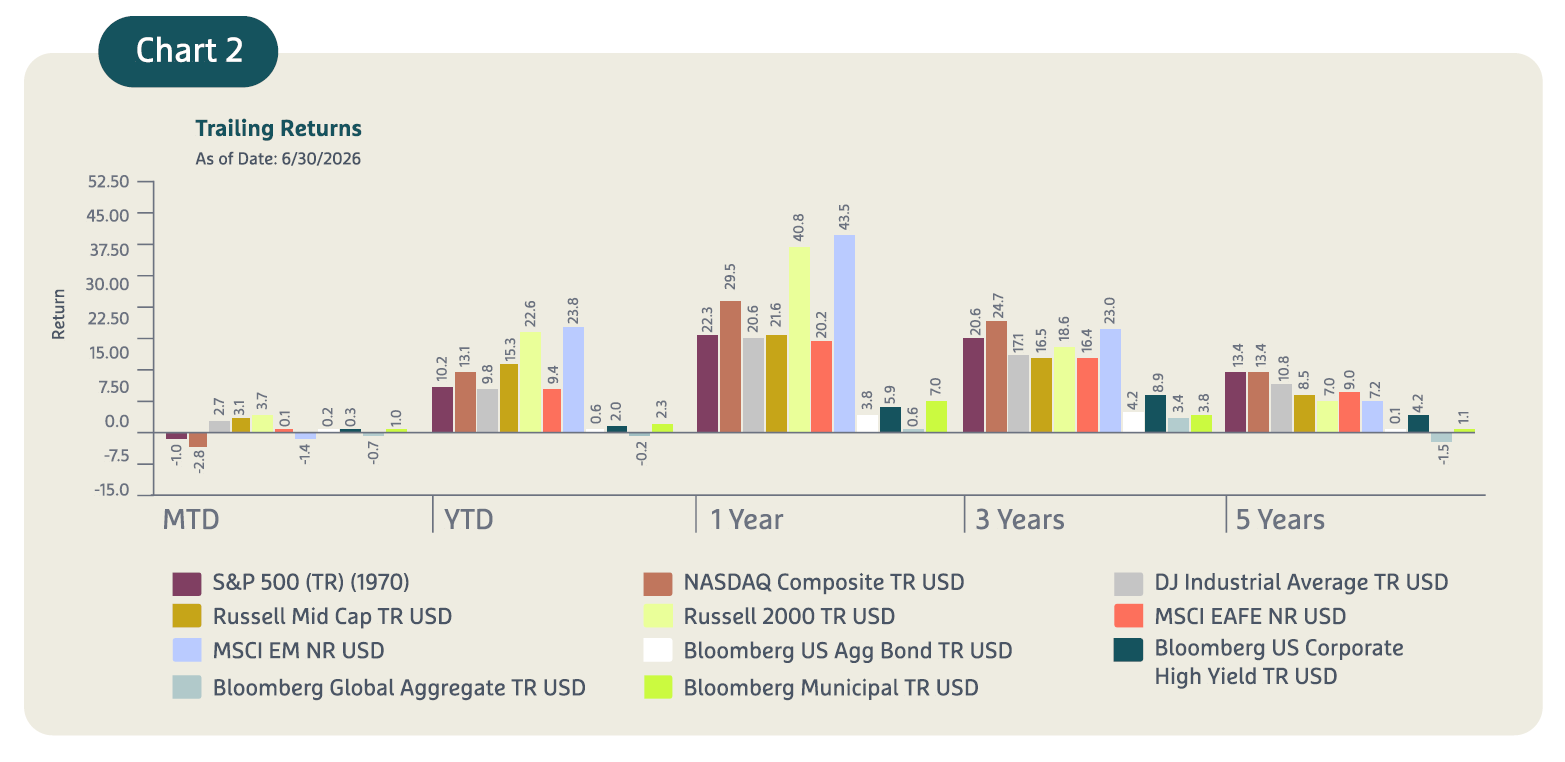

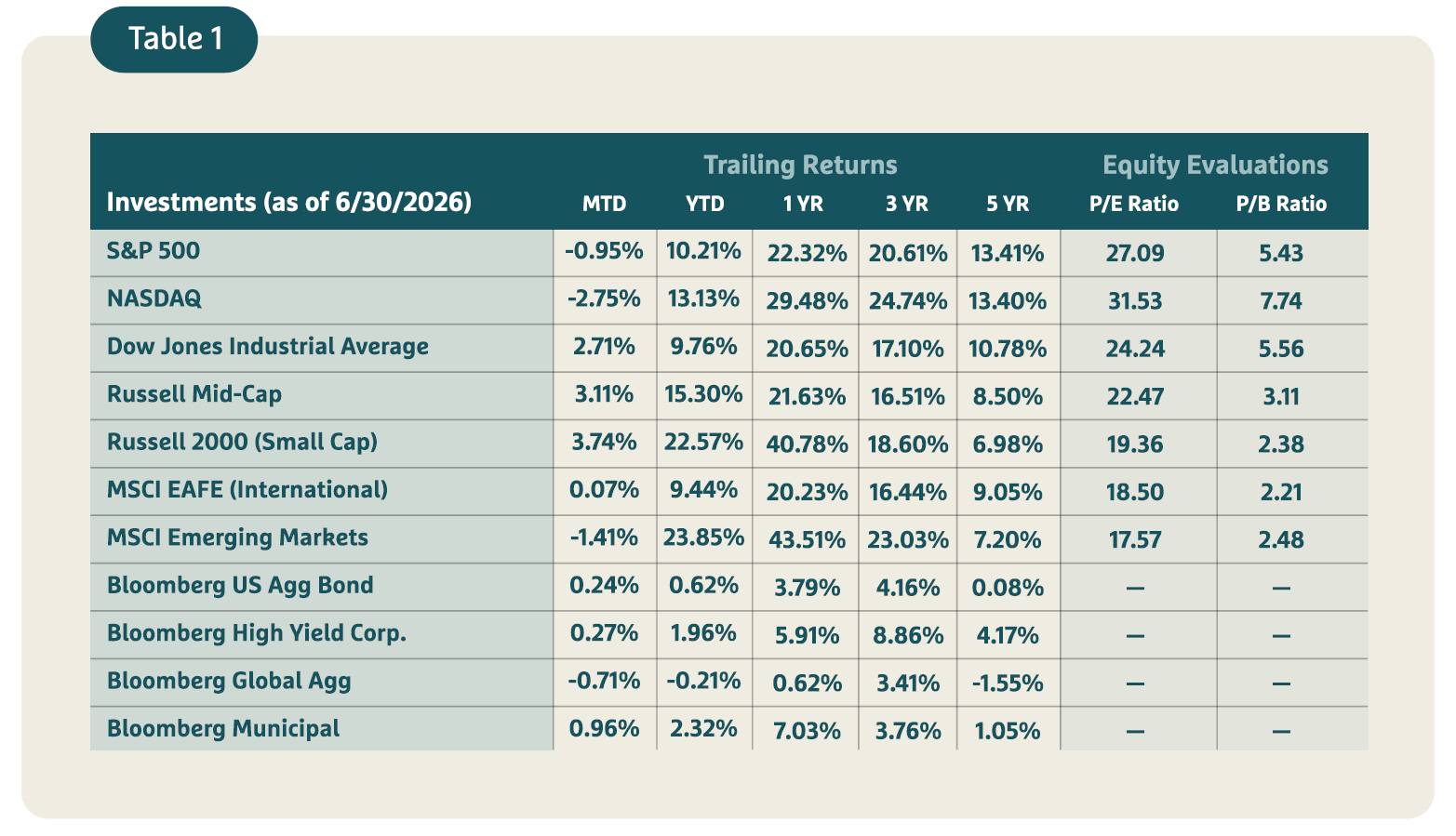

Market Update³

Market Review¹

Equities

Equities broadly felt the heat in the first month of summer. A multitude of questions around inflation, interest rates, and valuations plagued investors. Investors took profits and trimmed their holdings, particularly their domestic large cap growth after the rally seen in May and April. The S&P 500 returned -0.95% in June, and the NASDAQ returned -2.75%. There was reason for enthusiasm as the more value-oriented Dow Jones returned a positive +2.71%, and small caps returned +3.74%. Small cap companies continued to be the leader in the domestic equity market for the year, and are only overshadowed internationally by emerging markets, which did pull back in June, but remains the leader year-to-date. SpaceX officially became the largest IPO in history in mid-June and rapidly became one of the largest companies in the world, seeking to revolutionize space, and seek profits in its multi-faceted business model. Looking forward to the second half, investors are expecting solid economic growth and consumer spending to fuel earnings, which just finished a historically strong season. Although questions remain about the war in Iran, investor sentiment is high.€

Fixed Income

Fixed income delivered modest but positive returns in June, acting as a ballast to equities within a fully diversified portfolio. Yields rose slightly as inflation remains the focus of fixed income investors. The negative performance from rising yields was offset by high starting levels of interest that padded investors from losses. The Bloomberg Aggregate Bond Index returned +0.24%, and higher yielding bonds returned +0.27% outperforming their investment grade counterparts. The yield on a two-year treasury rose 14 bps as the Fed Funds Future alludes towards three rate hikes being more probable than one rate cut by the end of the year. Although rising yields can impact total return, it does offer an opportunity for investors to gain access to high quality bonds that have high levels of interest. On the year, the volatility in interest rates has led to nearly flat performance for fixed income investors, and the volatility is unlikely to subside in the second half, absent a clear direction on where inflation, and likewise interest rates, are headed.

Conclusion

Although markets broadly pulled back in June, the surrounding economic backdrop, and corporate earnings landscape continue to bode favorably for equity markets into the second half of the year. Investors also have the upcoming IPOs of both OpenAI, and Anthropic to look forward to in the coming quarters, as the AI trade looks to regain its momentum. Despite sticky inflation related to energy prices, the majority of consumers remain on solid footing and continue to propel spending and drive economic growth forward. Corporate investment in AI and its corresponding infrastructure are also positive tailwinds for growth in the coming quarter. All-in-all, economic data and financial indicators remain poised for strength in spite of some profit taking in June.

The statements provided herein are based solely on the opinions of the Osaic Investment Research Team and are being provided for general information purposes only. Neither the information nor any opinion expressed constitutes an offer or a solicitation to buy or sell any securities or other financial instruments. Any opinions provided herein should not be relied upon for investment decisions and may differ from those of other departments or divisions of Osaic Wealth, Inc. (˝Osaic˛) or its affiliates.

Certain information may be based on information received from sources the Osaic Investment Research Team considers reliable; however, the accuracy and completeness of such information cannot be guaranteed. Certain statements contained herein may constitute ˝projections,˛ ˝forecasts˛ and other ˝forward-looking statements˛ which do not reflect actual results and are based primarily upon applying retroactively a hypothetical set of assumptions to certain historical financial information. Any opinions, projections, forecasts and forward-looking statements presented herein reflect the judgment of the Osaic Investment Research Team only as of the date of this document and are subject to change without notice. Osaic has no obligation to provide updates or changes to these opinions, projections, forecasts and forward-looking statements. Osaic is not soliciting or recommending any action based on any information in this document.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss. In general, the bond market is volatile; bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed-income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Vehicles that invest in lower-rated debt securities (commonly referred to as junk bonds or high-yield bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. International investing involves special risks not present with U.S. investments due to factors such as increased volatility, currency fluctuation, and differences in auditing and other financial standards. These risks can be accentuated in emerging markets.

Index performance does not reflect the deduction of any fees and expenses, and if deducted, performance would be reduced. Indexes are unmanaged and investors are not able to invest directly into any index. Past performance cannot guarantee future results.

For Financial Professional Use Only: Securities and investment advisory services are offered through the firms: Osaic Wealth, Inc. and Osaic Institutions, Inc., broker-dealers, registered investment advisers, and members of FINRA and SIPC. Securities are offered through Osaic Services, Inc. and Ladenburg Thalmann & Co., broker-dealers and members of FINRA and SIPC. Advisory services are offered through Ladenburg Thalmann Asset Management, Inc., Osaic Advisory Services, LLC. and CW Advisors, LLC., registered investment advisers. Advisory programs offered by Osaic Wealth, Inc. are sponsored by VISION2020 Wealth Management Corp., an affiliated registered investment adviser.

1 Obtained from Bloomberg as of 6/30/2026

2 Consumption concentration may be up, adding slightly to economic fragility - Dallasfed.org

3 Returns obtained from Morningstar as of 6/30/2026

9002312