Made in America… Again

Introduction

After being gutted by production and labor offshoring for decades, suffering extreme sector contraction, and lagging the broader economy in recoveries, U.S. manufacturing is now showing early signs of a more durable rebound. The key question is whether this recent trend will be short-lived, as it has in previous episodes, or progress into a sustainable cycle supported by private investment, rising demand, and structural shifts in global supply chains. Together, these elements have the potential to usher in a manufacturing renaissance in the United States.

Manufacturing Origins

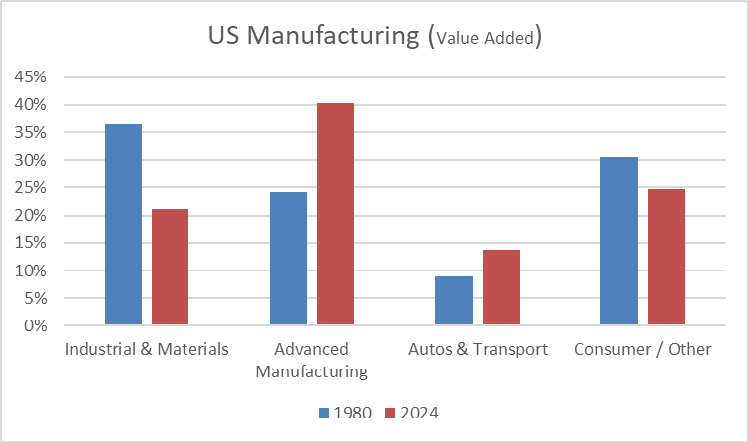

Before assessing the current resurgence in U.S. manufacturing, it is important to understand how the sector's composition has evolved. Decades ago, U.S. manufacturing was largely defined by heavy industrial, labor-intensive production. Outputs were primarily machinery, metals, and basic materials, as well as consumer goods, such as textiles, paper, and food products. Chart 1¹ shows that the mix has shifted significantly over time. Globalization incentivized lower-cost, labor-intensive production to move overseas, while advancements in automation reduced the need for labor in traditional industries domestically.

Chart 1 | US Manufacturing (Value Added)

At the same time, the U.S. increasingly specialized in areas where it held a competitive advantage, including innovation-driven, capital-intensive sectors such as semiconductors, pharmaceuticals, aerospace, and advanced chemical manufacturing. In addition to manufacturing accounting for fewer overall jobs than it did in the 1980s, certain industries within the sector have completely transformed. The U.S. has moved up the value chain, focusing less on volume-driven, low-margin goods and more on high-value, precision-based production. This shift helps explain why today’s manufacturing rebound looks different from past cycles, with growth increasingly tied to technology, intellectual property, and strategic supply chains rather than traditional industrial output.

Manufacturing Mania?

Recent data suggests momentum is building. The ISM Manufacturing Index is a monthly survey of purchasing managers that tracks key components of manufacturing activity, including new orders, production, employment, and supplier deliveries. A reading above 50 signals expansion, while a reading below 50 indicates contraction. The index is closely watched because it acts as a timely, forward-looking indicator of economic momentum, often signaling turning points in the manufacturing sector before they appear in hard data like Gross Domestic Product (GDP). The ISM Manufacturing Index has now expanded for three consecutive months for the first time since 2022, signaling a shift back to growth territory. While this alone does not confirm a full-cycle recovery, it reflects improving conditions across the industry.

At the same time, a surge in manufacturing investment is laying the foundation for longer-term growth. Roughly $1.6 trillion in announced industrial projects since the start of 2025 highlights one of the largest buildouts in decades, with capital flowing into semiconductors, advanced computing, pharmaceuticals, and energy infrastructure. The transition underway is not simply about producing more; it’s about producing differently. This transition reflects a critical competitive advantage in innovation, technology, and productivity rather than low-cost manufacturing. The current cycle is therefore not a return to the past, but an evolution toward a more advanced and specialized industrial future.

Government Stimulus

The recent wave of manufacturing investment is being driven by a fundamental shift in how companies approach supply chains and more supportive, strategically motivated government policy. At the corporate level, reshoring has moved from a theoretical concept to an active strategy. In recent years, geopolitical events have exposed the fragility of global supply chains, prompting companies to prioritize reliability alongside cost efficiency. Companies like Apple and Taiwan Semiconductor Manufacturing Company Limited (TSMC) have committed to over $400 billion in investments to build manufacturing capabilities at home and reduce overseas dependency.² Producing closer to end markets helps reduce transportation costs and mitigate geopolitical risks, while advancements in automation have made domestic production more economically viable despite higher labor costs.

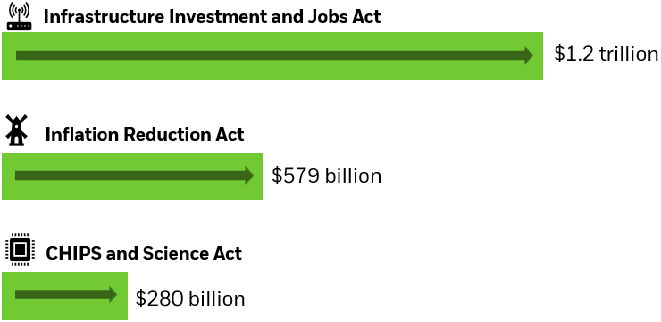

Government policy has played an important role in accelerating this shift. Chart 2³ shows that legislation such as the Infrastructure Investment and Jobs Act, the Inflation Reduction Act, and the CHIPS and Science Act have directed more than $2 trillion toward infrastructure, clean energy, and advanced manufacturing. Recent tax policy changes have further accelerated this trend through the One Big Beautiful Bill Act, which reinstated full expense treatment for equipment and R&D, allowing manufacturers to immediately deduct the cost of machinery, automation, and innovation investments. This effectively allows companies to lower taxable income while encouraging faster capital deployment.⁴ These incentives are lowering the cost of domestic production and supporting investment, giving U.S. manufacturers the tools to build, scale, and innovate with confidence.

Companies executing reshoring strategies are achieving 30-50% reductions in supply chain disruption costs and improving delivery reliability,⁵ and policy support is making those decisions more economically attractive. This combination is helping to drive a meaningful expansion in domestic manufacturing capacity.

Conclusion

The resurgence in U.S. manufacturing is not simply a cyclical rebound in activity, but the result of a multi-decade shift in what the country produces and how it develops those products. As the U.S. has grown beyond low-cost, labor-intensive manufacturing, it has established a leadership position in high-value, innovation-driven industries. The current wave of investment, supported by both private capital and public policy, reflects this evolution and reinforces the sector's positive long-term outlook. With capital being deployed at scale and supply chains being reoriented, the foundation for sustained industrial activity is taking shape. The next phase will depend on whether production and demand can rise to meet expanding capacity. Should that be the case, today’s momentum could be sustained for years to come.

Economic Definitions

ISM Manufacturing Index: The Manufacturing ISM Report On Business is based on data compiled from purchasing and supply executives nationwide. Survey responses reflect the change, if any, in the current month compared to the previous month. For each of the indicators measured (New Orders, Backlog of Orders, New Export Orders, Imports, Production, Supplier Deliveries, Inventories, Customers' Inventories, Employment and Prices), the report shows the percentage reporting each response, the net difference between the number of responses in the positive economic direction and the negative economic direction, and the diffusion index. A PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining.

GDP: Gross domestic product (GDP) measures the final market value of all goods and services produced within a country. It is the most frequently used indicator of economic activity. The GDP by expenditure approach measures total final expenditures (at purchasers' prices), including exports less imports. This concept is adjusted for inflation.

Disclosures

The statements provided herein are based solely on the opinions of the Osaic Research Team and are being provided for general information purposes only. Neither the information nor any opinion expressed constitutes an offer or a solicitation to buy or sell any securities or other financial instruments. Any opinions provided herein should not be relied upon for investment decisions and may differ from those of other departments or divisions of Osaic Wealth, inc. (“Osaic”) or its affiliates.

Certain information may be based on information received from sources the Osaic Research Team considers reliable; however, the accuracy and completeness of such information cannot be guaranteed. Certain statements contained herein may constitute “projections,” “forecasts” and other “forward-looking statements” which do not reflect actual results and are based primarily upon applying retroactively a hypothetical set of assumptions to certain historical financial information. Any opinions, projections, forecasts and forward-looking statements presented herein reflect the judgment of the Osaic Research Team only as of the date of this document and are subject to change without notice. Osaic has no obligation to provide updates or changes to these opinions, projections, forecasts and forward-looking statements. Osaic is not soliciting or recommending any action based on any information in this document.

Securities and investment advisory services are offered through the firms: Osaic Wealth, Inc. and Osaic Institutions, Inc., broker-dealers, registered investment advisers, and members of FINRA and SIPC. Securities are offered through Osaic Services, Inc. and Ladenburg Thalmann & Co., broker-dealers and members of FINRA and SIPC. Advisory services are offered through Ladenburg Thalmann Asset Management, Inc., Osaic Advisory Services, LLC. and CW Advisors, LLC., registered investment advisers. Advisory programs offered by Osaic Wealth, Inc. are sponsored by VISION2020 Wealth Management Corp., an affiliated registered investment adviser.

2 US Manufacturing Investment Tracker 2026 | IndustrialSage

3 Exploring the Rebirth of American Manufacturing | iShares - BlackRock

4 How New Tax Policy is Supercharging U.S. Manufacturing Investment | IndustrialSage

5 10 Reshoring Stats That Prove American Manufacturing's Edge

8882118